LONG ZDGE: Shareholder-friendly Management is en-route to transform this doozy into a multibagger via a restructuring and turnaround with compelling margin of safety in ZDGE.

This is part I of a series of writeups we aim to publish where we present the compelling margin of safety in ZDGE, where even a failed turnaround can result in a 50-250% share price appreciation.

We see pundits on Twitter yap about margin of safety and undervaluation- but what does it mean ? We think ZDGE symbolises all those attributes of a perfect investment, with a touch of long-activism from us.

ZDGE’s core business is resilient, and management is doing evetrything it can to bolster it up. ZDGE’s failing subsidiary however, needs help, and management launched a cost-saving program pertaining to it. In this deep-dive, we provide readers our reasons for which ZDGE, in a few years, will be a multibagger as per us, and we highlight the reasons why the stock price is down, and if management’s turnaround fails, we still see 50-250% upside in case of a divestiture. In part II of our writeup which will be released soon, we will provide management a roadmap to transform ZDGE from a Doozy into a multibagger. We also highlight how easy it is for a shareholder friendly management, like the present ZDGE management, to transform Gurushots into a money-maker- even if they don’t follow our guidelines.

We also point out the margin of safety- about 50% of the market cap is net cash with miniscule debt- with virtually no possibility of a bankruptcy! In our humble opinion, if management is smart, this investment is so safe that our bear case scenario in an efficient market is up 50% if the turnaround doesn’t work!

Investment thesis Summary:

Core Business Resilience: Zedge operates a steady and cash-generating phone personalization app business, contributing significantly to its revenues despite the fading COVID-era demand spike.

Low Valuation & Margin of Safety:

Valuation metrics are extremely attractive, with a Price-to-Sales ratio of 1.26 and an EV/EBITDA of 12x, indicating a heavily discounted stock.Strong balance sheet with $20 million in cash against a $38 million market cap, providing a significant margin of safety.

Past Challenges: The ill-fated Gurushots acquisition temporarily dragged earnings into negative territory due to high costs and impairment charges. However, these write-offs are complete, removing a major overhang on the stock.

Turnaround Potential:

Management has announced a 14% workforce reduction, focusing on Gurushots cost containment, signaling a renewed commitment to profitability.

Gurushots is now a low-risk "call option" within the company, since ZDGE has written off virtually all of Gurushot’s asset value that needed to be removed from its books. Even though Gurushots contributes to almost 100% of ZDGE’s operating losses, effective monetisation and earnings growth from Gurushots can help turn ZDGE into a multibagger.. In the part II of this Writeup, Ragnarok Research will give a blueprint that management can use to turnaround and restructure Gurushots!Value-Generating Initiatives:

Management is bolstering core business via strategic use of AI to enhance the core business by offering innovative phone customization options (e.g., AI-generated ringtones and wallpapers).

Aggressive share buyback programs—$5 million approved—retiring up to 13% of outstanding shares at current prices.

Investment Safety: Even in the worst-case scenario, where Gurushots fails to turn around, a divestiture would substantially boost profitability and unlock shareholder value, which we estimate will drive share price 50-250% higher if management gives up on the turnaround and divests gurushots.

Easy path for management: In this writeup we emphasise how clear of a path management has to implement a turnaround. In Part II, we will release steps management can take, after extensive DD- via testing of the gurushots platform, and conversations with users. Gurushots is a beloved brand in the photography community, especially amateurs, but they hate the pay-to-win aspect of Gurushots and if handled properly, which we believe management will do- especially if they follow our research and guides- will result in a multibagger.

Compelling Upside: ZDGE is an undervalued stock which holds a key hidden underperforming asset which management is eyeing to bring back. A turnaround is definitely possible because all that needs to be fixed is the monetisation of gurushots and incentives. In the off-chance that this doesn’t work, ZDGE has a huge margin of safety due to its strong balance sheet, and a resilient core business, which if ZDGE focuses on solely by divesting gurushots, is worth about 50-250% more than it is valued today.

Introduction

Zedge is a 38-million dollar company, valued 12x EV-EBITDA that makes an wallpaper app that you find in google play store, for which you can pay a small amount for custom animated wallpapers, and phone personalisation in general.By phone personalisation, we mean custom notification sounds, wallpapers, ringtones, etc., It isn’t a high-tech, attractive software company, which is partly the reason that it trades at a low valuation (1.26 Price-to-sales, and 8 Price-to-cash). The share price paints a story:

The stock started surging at 2020, the covid era, when bored users started splurging money on ‘phone customisation’, and as the covid hype faded away, the stock cratered. This is where the market made a mistake. The market correlated the stock directly to covid spending. For example, look at ZDGE’s revenue graph:

Revenue has been steadily rising even after covid effects subsided. In fact, it has tripled since 2020.

But then, surely the market can’t be this stupid, right ? Well, investors first sold ZDGE stock for the covid hype fading, but didnt buy them backdue to Its earnings:

Also its Operating income:

Earnings quickly took a dive and is accelerating down due to an explosion in costs. Operating income 153k in FY 2024, while net income was -9M- mainly due to impairment charges related to the gurushot acquisition(Ebitda was 2.6M in FY 2024). An unprofitable software company(accounting for writedowns) with negative sentiment is a recipe for low valuations, which is reflected in the stock price.

What went wrong ?

The sudden dip in earnings caused by one primary factor: The gurushots acquisition. In April 2022, ZDGE announced that it was acquisiring a company called gurushots. Now gurushots, which you can see for yourself here, is a photography game. It is a pretty good concept- where users compete on who takes the best photos and you ‘move up the ranks’ with different badges. While this is a great concept for aspiring photographers, gurushots is not a moneymaker. The thing about acquisitions is you get a new revenue stream … but in the expense of new costs (salaries of new employees, integration costs, etc.). In ZDGE’s most recent quarter, ZDGE earned 7 million in revenues, of which just 644k was attributed to gurushots. That is basically peanuts as far as materiality goes. In the yearly scale, we see the following proportions:

Dark blue being normal Zedge core business, and light blue being Gurushots.

But we suppose it is not all that bad because gurushots is contributing something to revenues. However, the catch is it is contributing a lot to the costs:

These are figures from ZDGE’s most recent quarter. Earnings this quarter was -457k. However, if we pretended Gurushots did not exist, ZDGE’s income from operations would have been +934k! About 1.3 million more! And this is not counting the exorbitant impairment charges ZDGE has been taking! However, management in FY 2024 10-K revealed that the write-downs related to gurushots are basically over:

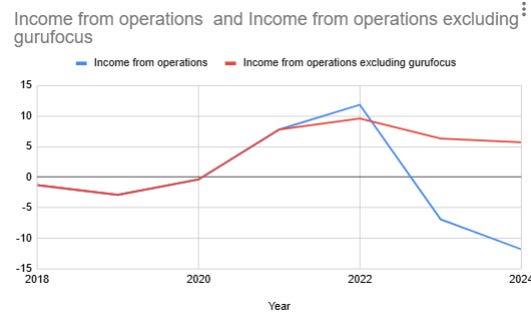

Recall how we saw a sudden dips in operating income starting 2023 ? Here is what the chart of ZDGE’s income from operations chart would look like, had ZDGE not acquired gurushots:

Blue: Present Income from Operations of ZDGE

Red: Income from operations without gurufocus

Because of the acquisition, we have seen earnings tank into the negative territory, with management, in FY 2024, taking a 11 million dollar impairment charge relating to gurufocus(which will not happen going forward), not to mention Operating income dipping from about 9 million in 2022 to 153k in 2024 due to the huge SG&A costs related to Gurushots.

But the funny thing is, the PE ratio(here, definition being market cap/net income) had the gurushots acquisition not have happened, would have still been a meagre 6.71(as of FY 2024, if we discount loss from operations from gurufocus, along with its related impairment charge), or more recently 10.17(as of latest quarter, annualised) … a criminal undervaluation for a software company… not to mention ZDGE has 20 million dollars worth of cash against a 38 million dollar market cap, with just about 200k in debt, bringing Price-to-cash to more than 50% … Talk about a ‘safe’ investment!

So … we have a core business which is pretty resilient so far, which is being weighed down by a bad acquisition.… But we believe management can nullify every single thing that is keeping the stock down pretty easily.

The value creation opportunity

Based on the facts stated above, it is clear that the main problem with ZDGE is Gurushots. Now, the two things ZDGE could do is either divest Gurushots, or turn it around and bring back earnings and revenue growth. Below, we dig deeper into each of the value-generating moves we believe ZDGE should make. To be clear, we think ZDGE should/would pick the latter option.

Divest/Sell Gurushots. Impact: Highly positive. Likelihood: Almost 0

Just to be clear, our long-term plan for ZDGE would be to turnaround Gurushots to turn it into a money-generating machine. We want to highlighted divestiture as an option to show how even the worst-case scenario of the gurushots turnaround not working can be a great thing for the share price via a divestiture. This is a great margin of stock since even the worst-case scenario of gurushots would yield a share price appreciation for ZDGE.

Say ZDGE’s turnaround doesn’t go as hoped and management wants to get rid of Gurushots. What happens then ?As high highlighted earlier, ZDGE’s PE ratio without gurufocus is at an outrageous 6x(FY 2024- stripping out gurushocus related impairment and amortization charges and SG&A) or 10x(As of latest quarter annualised). Now that management has already pointed out that there won’t be such large write-downs going forward because about 100% of the assets related to gurushots have been written off, Gurushots is basically a sitting duck:

The only thing Gurushots is contributing to ZDGE, it its sky-high operating expenses such as Gurushots’ employees salaries, etc. The market hasn’t been valuing ZDGE properly because it views ZDGE has a decelerating software company which made a blunder of an acquisition with miniscule operating income, while failing to see the resilient core business. If we strip ZDGE off of Gurufocus via a sale or divestiture and get rid of its operating costs(like SG&A, salaries… etc), we believe the market will re-rate Gurufocus from a 6x to atleast a conservative 15x PE ratio, representing a 50-250% gain from current price levels, mainly due to the realisation that operating income would jump from 0.15million to about 5 million immediately, assuming FY 2024 numbers. Refer to the following chart again:

This is a conservative estimate, considering that a company which has a growth runway (more on this in the next point) ,and flipping into positive earnings is a narrative the market has historically loved. In fact, ZDGE’s EV/EBITDA ratio stands at an attractive 12x, even though EBITDA is set to grow when/if Gurushot’s SG&A base vanishes after the sale/divestiture. The valuation is not the only aspect of this decision. Divesting Gurushots will allow management to focus more on the core business, helping them bring growth back to Zedge’s core business using AI, which I address further below in the writeup later.

However, management is hellbent on not shutting down gurushots, and instead turning it around. Look at CEO’s remarks as of most recent earning call:

This is not to say that management might not consider a divestiture in the future, but I don’t believe we can expect it in the short-term. However, with all the Gurushots related write-downs over, it is fair to give management a shot at turning this dud around, especially considering that they said they have taken steps in the past 6 months or so. The good part is, if management fails to turnaround gurushots, they still have a very undervalued core business, and they can divest Gurushots as a last resort and it would still result in a share price appreciation. More about the Gurushots restructuring below

Gurushots’ Turnaround plan: Management has already announced plans to restructure gurushots and cut costs via reduction of employee headcounts, and also look for ways to overhaul Gurushots to become a growth machine.

With all the write-downs and impairment charges relating to the Gurushots over, Gurushots basically acts as a ‘free call option’ within the company since its asset value is virtually 0. This is amazing because Gurushots is this entity that is worth nothing, but contributes a LOT to ZDGE’s costs. Even if ZDGE cuts SOME of gurushots’ costs, it will help ZDGE a disproportionately amount… and in the case of a total turnaround of gurushots, we can see ZDGE becoming more than a 5-bagger. The best part is even if the turnaround fails, divestiture, as mentioned above, will unlock shareholder value.

On the 21st of January 2025, management announced a restructuring plan to reduce ZDGE’s headcount by 14%, mainly by letting go of Gurushots employees. This is the stripping of costs we were talking about:

Gurushots’ acquisition has contributed so much to ZDGE’s SG&A expenses, and it is one of the primary reasons ZDGE’s operating expenses is miniscule. After layoffs and a sort of ‘leanification’ of Gurushots, management is improving the bottom line of income statement of ZDGE, while preserving the option to exponentially improve both the topline and the bottom line

Next, the restructuring plan involves other cost-savings which will save 1.7 million in pre-tax(this incoludes the layoffs), which implies about 15% of FY 2024’s pre-tax losses(Pre-tax income was -11.37). This makes our analogy of a free call option even better- management seems to be focused on lessening the drag impact Gurushots seems to be having on ZDGE, while preserving all possibility of a turnaround and turning Gurushots into a growth machine!

Other than a divestiture, this will be the highest value-generator for ZDGE in our opinion. Gurushots cannot make money for the life of itself at the moment- but if that changes, we can see a world’s worth of multiple expansion. So- management knows how to cut costs by firing people and lowering user acquisition costs, but what about actually inducing growth to Gurushots ?

Yes, management does say that they are still figuring out the roadmap to turn-around, but Ragnarok Research has done due diligence on this topic and webelieve that Gurushots is one of those ideas that are great for the photographic community, but just hasn’t found the right way to monetise yet. When ZDGE did try to monetise it, players started complaining of it becoming a pay-to-win. Now, management wants to fix it and are confidence about their options. This attitude can be seen in management’s reluctance to divest or shut down Gurushots- because it is a strong brand in amateur photography!

Best part is, management plans to attack this monetisation problem directly:

As stated, Zedge wants to overhaul gurushots and rethink its entire monetisation policy and make a new player experience. This is a step in the right direction, and it is almost undeniable proof of how shareholder-friendly management is. Our main conviction in Gurushots’ turnaround is that the problem is clear: the concept of a competition for amateur until Gurushots became a pay-to-win. This is not a very hard problem to fix because the concept is great and photographers even agree. Look at some trustpilot reviews:

In Part II, we will touch up on how management can actually turnaround Gurushots.

To be clear, we have full confidence in what management will come up with- and this is just our 2-cents. Even if management does not take the steps we list out, we will remain long because management’s docs is at a turnaround of gurushots and cutting costs- which is all we ask for.

Other Value-Generation views management is pursuing right now:

ZDGE has a fairly competent management team, which is doing everything it can to help out shareholders by taking measures to unlock shareholder value in other avenues as well. Here are some of them which makes us confident that ZDGE is a good long-term investment, assuming ZDGE handles Gurushots in either of the two ways highlighted above.

Accelerate growth of ZDGE’s core business. Impact: Positive. Likelihood: Almost 100%

We see great growth opportunities ahead of ZDGE, especially after the most recent earnings call. We all know how Generative AI is taking the world by storm- from Sora, to ChatGPT, etc. ZDGE wants to capitalise on this opportunity. Instead of offering plain wallpapers and sounds to users, ZDGE is transitioning into a paid model where users themselves can create and customise their own sounds and pictures. This sets ZDGE on a path to capitalize on growing AI trends where users are virtually paying for an AI-agent that streamlines the process between giving a prompt, and embedding the end result to your phone via wallpaper, ringtone, or notification sounds:

A valid concern an investor may have is ‘wait, why can’t I use something like Sora myself, and use that as my wallpaper?’. Well wallpapers aren’t the only offering of ZDGE. It specialises as phone-customisation specific products, like AI-made ringtones(Will roll out soon as per management), custom app icons … things that are hard to integrate from an image to the UI of a phone. ZDGE merely streamlines that process.

The most recent quarter actually suffered a decline in advertising revenue due to a one-off, which has been rectified:

So, our latest quarter annualised PE ratio of about 10x is actually inflated due to a one-off advertising bug and some ‘integration complexities’ from adtech partners which is supposed to normalise going forward. Goes to show how undervalued the company is. This decision by management, according to us, will further bolster ZDGE’s core business. Returning growth back to ZDGE’s business can be better done if management is solely focused on the core business, instead of dividing attention between the core, and gurushots. So, we believe this action goes hand-in-hand with the divestiture/sale of gurushots.

The value generation classic that management is already implementing: Share buybacks. Impact: Positive. Likelihood: Almost 100%

A classic maneuver in the value generation playbook is ramping up buybacks- and the best part is, this is exactly what ZDGE is doing. ZDGE recently just approved a 5 million dollar share buyback program:

This is extremely bullish in our opinion, considering ZDGE just completed a 3 million dollar share buyback last july. This just goes to show how confident management is in their strategy. Even if we disregard that, a 5 million dollar share buyback would retire, roughly 13% of the shares at current prices, making the company even more undervalued and even more primed for share appreciation when funds start valuing it as a profitable, and growing company, assuming the two steps above are also successfully taken.

Risks

One of the main risks to the thesis is Gurushots not turning around as we hoped- but that is also a pillar of the investment thesis. Even if it does nt work out, a divestiture will be extremely value-generative due to the market likely performing a multiple-rerating to price in the resilient core business of Zedge.

Conclusion

We have not seen a company like ZDGE in a long time. This is a software company valued 12x Ev-Ebitda, but with an extremely depressed Ebitda which management is working hard to fix. Soon, market will catch up like it always does and we believe that this has multibagger potential. Sure, the actual turning around of Gurushots might be hard, but even if it all doesn’t work out, it ends well for ZDGE. In our view, this makes ZDGE a strong, screaming buy.

In Part II, we will release a set of guides we think management should/will take to transform solely gurushots. This writeup was to highlight the attractive opportunity in the total entity, which is Zedge Inc,. Nothing more. The part II will be way more comprehensive. An activist bet can’t be made on ZDGE because a majority stockholder controls virtually 70% of the voting rights, so activism isn’t really an option- however sending out Part II into the ethos in hopes that management reads it and gets some inspiration is our goal- other than a fun little exercise to challenge ourselves.

Very interesting idea. Thank you for sharing. Here are some of my thoughts.

Most important:

#1 What do you think about the deteriorating fundamentals for Zedge App? MAU are decreasing >10% YoY - down to 25M in Q1-2025 from 33M in Q1-2023.

Though it is balanced out by increasing revenue from subscribing users. I could see the AI creator feature as a strong tailwind here. Though using it briefly, I was put off by its result.

Further more

#2 Not as important but: Emojipedia.org is carried along with 5.4M - Is it really worth 5.4M? It has 5k app downloads in the play store and no revenue is reported for this division in the latest 10-k. So there is potential for additional write-offs up to 5.4M.

#3 Gurushots seems dead. 1.5 stars on Trustpilot. People are not only complaining about the monetization but also the product itself. A lot need to happen to turn this around.

Positive:

#3 Subscription revenue is inceasing - also displayed in the strong increase in the changes in subscription deferred revenue. ($594k vs $163k YoY)

Conclusion: I agree w your valuation metrics. 20M in the bank. 8-9M FCF at a 41M valuation leading to 2.5x EV/FCF Or 5x EV/ Fwd earnings. But not yet sure how to think about the falling MAU >10% YoY